Izak Odendaal, Investment Strategist at Old Mutual Wealth

The title of this article was also that of a famous 1919 book by the great John Maynard Keynes. He argued that the Treaty of Versailles, which officially brought an end to World War I, imposed such economic hardship on Germany that a European financial collapse and another war were virtually inevitable. He would be proven catastrophically right on both counts. In contrast, the Memorandum of Understanding between the US and Iran – signed by US President Trump on Wednesday, also at the Palace of Versailles – is unambiguously good news for the world economy. However, it does little to salvage Trump’s reputation or American foreign policy credibility.

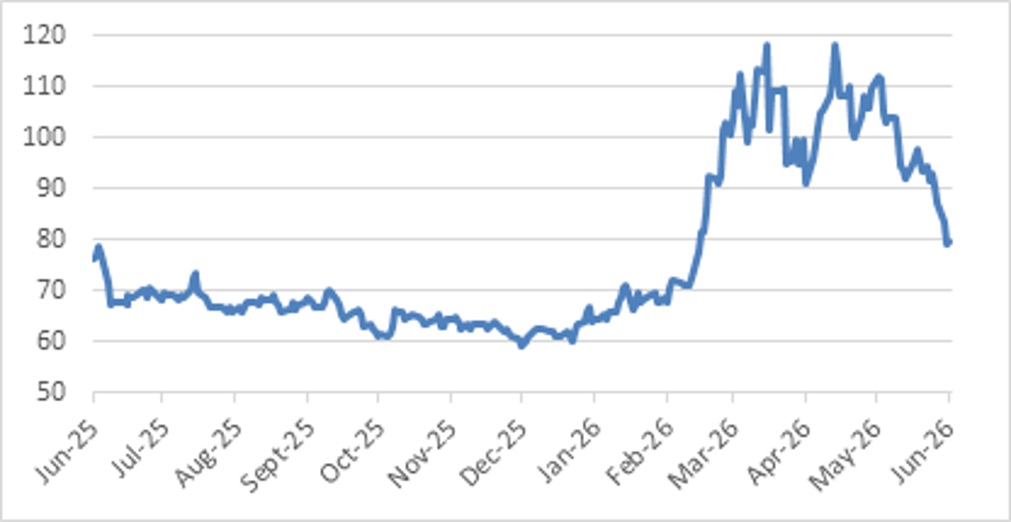

An MoU does not, of course, guarantee peace. Flare-ups and incidents remain likely in the 60-day period while both sides negotiate the thorny issues related to Iran’s nuclear programme. Indeed, the first roadblock was hit over weekend when Iran claimed to close the Strait of Hormuz again in response to ongoing fighting between Israel and Hezbollah. What lies beyond the 60-day period is also unknown. Nonetheless, reaching an MoU strongly suggests both the US and Iran want to put the war behind them. At any rate, markets didn’t wait for the finer details – they rarely do – and immediately started positioning for a post-war world which includes a gradual reopening of the Strait of Hormuz. In fact, this repositioning started weeks ago already, another reminder of how difficult it is to time the market. The upshot is that crude oil tumbled to $80 for the first time since March on Friday. This move might be a bit overdone given the uncertainties, but few will complain since the price is now well below the late April peak.

Chart 1: Brent crude oil price, $ per barrel

Source: LSEG Datastream

However, it is still higher than at the start of the year, squeezing household purchasing power and company margins. The relief won’t necessarily be felt immediately, just as the impact of higher prices wasn’t, as businesses don’t change orders, hiring or pricing plans overnight. In South Africa specifically, we’ll have to wait until next month for retail fuel prices to decline. Even then, the fall will be tempered by the fuel levy rising to its normal level. Still, petrol is on course to drop around R1.50 per litre and diesel by R3 per litre in the first week of July.

From an inflation point of view, the reported numbers are backward-looking. Most countries have only released May data, a period when oil prices averaged around $100. It is only by July that reported inflation will start looking better. However, because the oil price fell sharply during the second half of last year, there is unfavourable base for the remainder of this year, keeping inflation rates somewhat elevated. It’s important to remember that inflation always compares current prices with a period in the past, usually 12 months earlier.

Fighting the last war

This will still cause concern among central bankers who worry that inflation expectations could become unmoored, in other words, that households and businesses might believe that temporary inflation will become permanent. Central banks are often accused of fighting the last war. Put differently, they tend to be haunted by the last policy error made. Most underestimated the post-Covid inflation surge and waited too long to act. This time round, faced with elevated inflation, and the risk that price pressures broaden from fuel to other goods and services, several central banks increased interest rates. Others have adopted a wait-and-see attitude. Only time will tell which approach is right. For those that hiked, oil price relief will not lead to an immediate reversal of these changes, and indeed some central banks might choose to plough ahead with a few more hikes.

Among major central banks, last week saw the Bank of England, Swiss National Bank and Bank of Canada maintain interest rates, while the European Central Bank (ECB) and Bank of Japan hiked. The ECB lifted its policy rate from 2% to 2.25%. It is famously (or infamously) sensitive to energy prices, and hiked rates in response to higher oil prices on the eve of both the 2008 and 2011 crises. It was quickly forced to reverse those increases. However, with the European labour market being relatively tight, the risks of a wage-price spiral remain, and the market is pricing in another 25-basis point hike.

The Bank of Japan is on a very gradual path to exit two decades of near-zero interest rates. Even after last week’s hike, its policy rate is still only 1%. Arguably, it would have been hiking rates regardless of the Iran war, though with the yen still weak and Japan an energy importer, it was treading a fine line.

Warsh and Peace

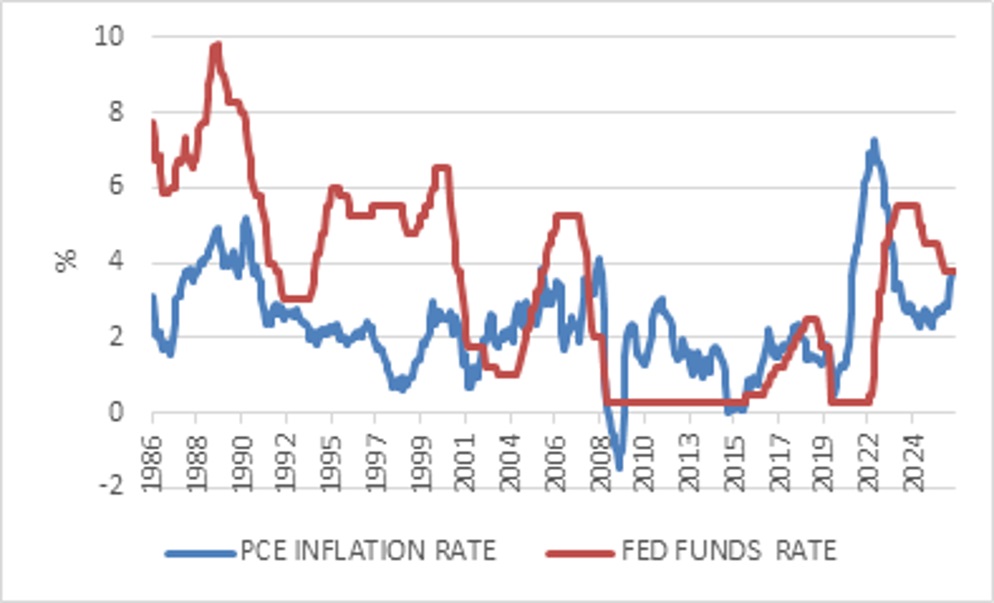

The most important central bank remains the US Federal Reserve. Last week’s policy meeting was the first under the leadership of the new Chair, Kevin Warsh. He will have been particularly relieved to learn about the ceasefire, as it reduces the urgency to act. US inflation has been above the 2% target since early 2021 and has recently moved further away from the target.

Chart 2: US interest rates and inflation

Source: LSEG Datastream

While rates were left unchanged as expected, the meeting outcome still moved markets, especially the dollar, which jumped to the highest level in a year. Warsh came into the job with strong views on how the Fed should change, but also facing the accusation that he would do Trump’s bidding and lower interest rates. His first meeting showed indications of the former but no sign of the latter. The dramatically shortened statement reaffirmed the Fed’s commitment to price stability and dropped the suggestion that the next move would be towards lower rates.

Warsh has long criticised the Fed for overcommunicating, and it is likely that he will scale back press conferences, for instance. He declined to participate in the so-called dot-plot that summarises the anonymous forecasts of Fed officials. This renders it much less useful, though it is still notable that several officials now believe rates should be higher at year-end, whereas none did when the March dot-plot was published.

He has also set up five task teams consisting of experts inside and outside the Fed to work on the size of its balance sheet, communication strategy, alternative data sources, the framework through which it analyses inflation, and productivity and jobs. The latter is presumably in line with his past comments that artificial intelligence will result in a massive productivity boom that will drive inflation and ultimately interest rates lower.

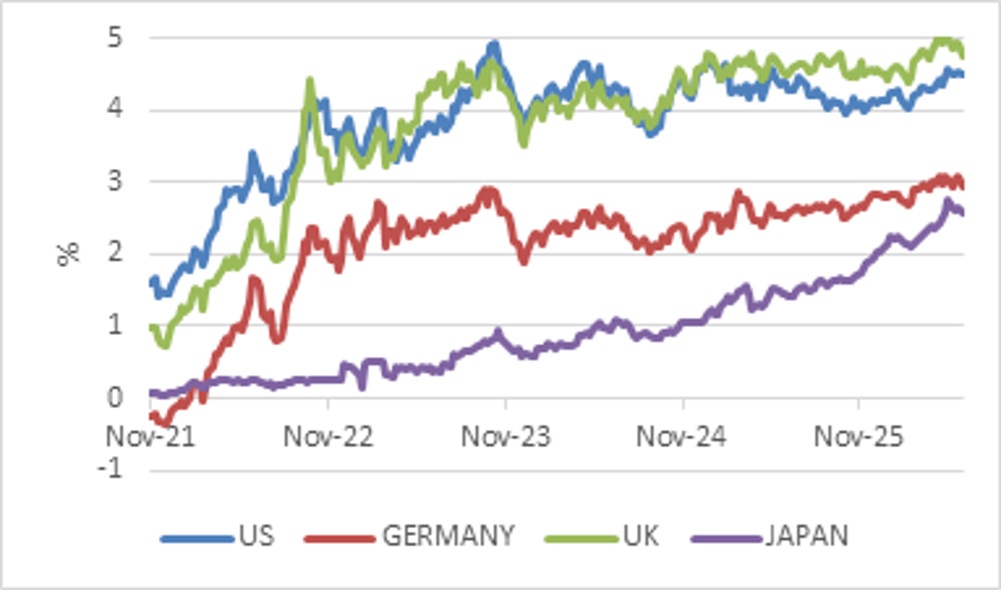

Chart 3:10-year government bond yields

Source: LSEG Datastream

In the nearer term, however, higher rates cannot be ruled out if the US economy maintains solid momentum and non-fuel inflation remains elevated. The market is now pricing in a hike by year-end, but this might be an overreaction since Warsh emphatically tried to say as little as possible about the Fed’s future plans. Technically inclined readers will note that, while US government bond yields are higher over the past few days, the expected inflation rate derived from the difference between nominal and inflation-protected yields, the so-called breakeven inflation rate shown in chart 4, has declined.To put this in plain English: the market seems less worried about inflation and more concerned that the Fed’s reaction to inflation has changed. This seems premature.

Chart 4: Breakeven 10-year inflation

Source: LSEG Datastream

Higher-for-longer

Nonetheless, the fact that bond yields across developed markets remain above pre-war levels despite the plunging oil price reflects the reality that the world has changed. It is no longer the demand side (specifically the post-2008 demand shortfall) that is setting the pace, but the supply side. Supply constraints, bottlenecks, chokepoints and security requirements are now top of mind. Addressing this requires investment, whether it is in AI datacentres, defensive capabilities, windfarms, oil pipelines, or storage facilities. The Hormuz crisis has yet again illustrated the need for resilience and a “just in case” mentality. This is a big shift from the focus on efficiency-through-outsourcing and the disinflationary “just in time” supply chain management of recent decades. All this investment spending comes at a time when government borrowing remains elevated. It shifts the balance between the demand for and supply of savings in the global economy and therefore raises the so-called neutral real interest rates. While interest rates will always be cyclical, bobbing up and down, they will generally be higher over the next decade or so compared to the previous 15 years.

This is also reason to be somewhat circumspect over the elevated valuations in parts of the global equity market. For now, AI enthusiasm is solid and profit growth strong, but ultimately capital flows to where the better risk-adjusted returns are. Higher rates could start to look attractive relative to equities at some point, at a time when blockbuster listings and new share issuance to fund capex are also competing.

What does this mean for South Africa? First, as a net importer of oil and petroleum products, the ceasefire is good news. However, what peace gives, a hawkish Fed might take away by putting downward pressure on precious metals prices and the rand. So far so good, though.

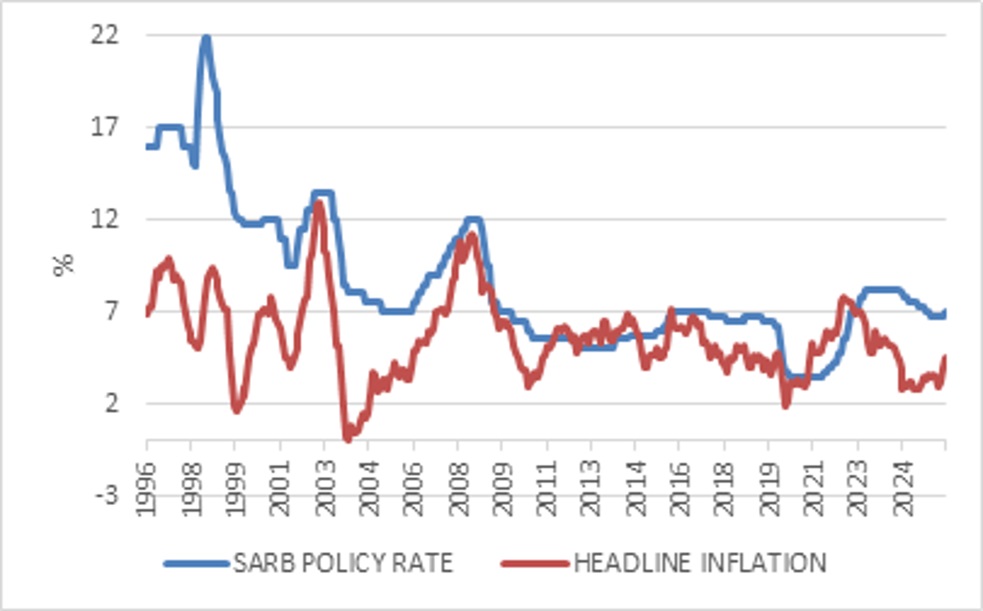

In terms of the interest rate outlook, it is important to separate cyclical from structural trends. The current cycle should be very short-lived. The latest inflation statistics for the month of May showed headline inflation rising to 4.5%, the highest level in two years but a bit less than expected. The biggest culprit was predictably fuel inflation rising to 28% year-on-year. June petrol inflation will be even higher but will mark the peak. By the end of last week, the rand oil price was flat compared to a year ago. Since it was low in the second half of last year, the base for year-on-year comparisons will be unfavourable for the next few months. However, by early next year, petrol inflation could be negative again and start pulling headline inflation down towards the 3% target next year.

Beyond fuel, core inflation ticked up to 3.8% but the monthly increase was modest at 0.2%. There are a few obvious signs of second-round effects in the data. This could change, and of course there are the risks to food prices from El Nino. However, the Reserve Bank’s policy rate is already at 7% and in restrictive territory with room to absorb potential shocks. Therefore, there is no need to raise rates at the July Monetary Policy Committee (MPC) meeting unless something dramatically changes the inflation outlook between now and then. Rate cuts should come early next year.

Chart 5: South African inflation and interest rates

Source: LSEG Datastream

Structurally, interest should continue to grind lower, and the trend over the next decade or so therefore looks different to major developed markets. In fact, we are likely to experience a bumpy process towards converging inflation and interest rates between South Africa and developed countries. Achieving a 3% inflation target over time should be very positive for South African bonds and rate-sensitive equities, which remain priced as though long-term inflation will be much higher. A lot needs to happen to get this right, but the Reserve Bank is committed to its target. It is not a war, but it is a battle worth fighting. Investors need to take it seriously too.

ENDS